The Machine Can Price It. It Can't Tell Me It's Mine.

By Conny Lazo

Agentic Engineer. Project Manager. Shipping software with AI agents.

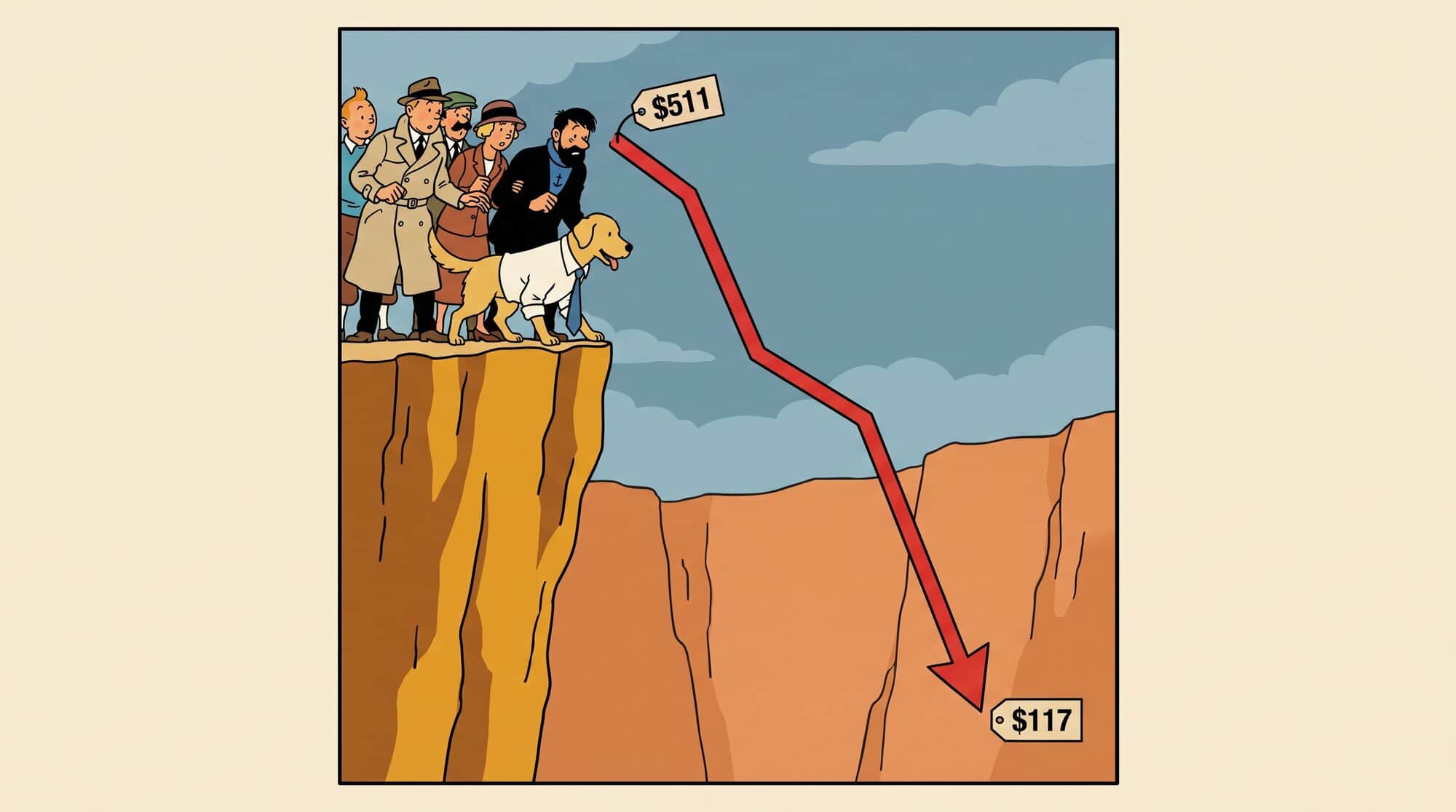

There is a stock that fell out of a window.

In December 2023, one share of Lululemon — the yoga-pants company — cost $511. Last week it cost $117. That is not a dip. It has lost more than three-quarters of its value. One day last June it dropped 20% before the market closed.

When something falls that hard, two kinds of people come to look. The first was Michael Burry — the investor Christian Bale played in The Big Short, the one who got famous betting the whole house was about to burn down. He wrote the company up. His pitch, more or less: it's the only American clothing company of any size you can buy for less than ten times what it earns in a year — meaning the whole thing would pay for itself out of profit in about a decade. That's cheap. Famous brands usually cost two or three times that, because people pay up for a sure thing. And a wonderful business — fat profits, loyal customers, steady growth — on sale at a marked-down price is the exact thing a value investor lives to find. The second was a fellow who teaches regular people to invest like Warren Buffett. He likes it too.

A doom-and-gloom short-seller and a cheerful Buffett teacher, agreeing — of all things — about the same pile of leggings. One of them has a line for it: bad management is a value investor's best friend.

And oh, the management. This is a company whose founder once printed "Who is John Galt?" — a line from an Ayn Rand novel — on the shopping bags. For yoga pants. In 2013 it recalled a batch of leggings for being see-through, and the founder went on television to explain that the real trouble was that "some women's bodies just don't actually work" in them. He then apologized. To his employees. Not, you'll notice, to the women.

So the stock is cheap, the company is a circus, and two famous investors are circling. That got my attention. So I did the only thing I know how to do. I fed it to my robot.

My robot is a value-investing tool I've been building. You hand it a company; it reads the boring paperwork — years of it — and tells you what the business is really worth, and whether today's price is a deal.

It chewed on Lululemon for about two hours and lit up green. BUY.

It wasn't shy. It put the company's fair value — what a share ought to cost, if the world were being reasonable — at $397.

That number isn't pulled from the air. You start with what the company earns per share today, and estimate how fast that grows over ten years — which tells you what it'll earn a decade out. You stick a sensible price tag on those future earnings, and now you've got a share price for ten years from now. Then you run it backwards: what would you pay today to turn that into about 15% a year, the return that makes the risk worth it? That backwards number is the fair value. Here, $397.

Then the part I like. Because every step in that chain is a guess, and guesses are wrong all the time, you cut the answer in half before you'd dare buy — call it $198. Pay that or less and you've left yourself room to be wrong and still come out ahead. Today the stock goes for $117, under even that. By the tool's own rules, that's a ten-dollar bill on sale for three.

There's a catch, and it's a big one. The math grades the company on the last seven years — and the last seven years were a party. Revenue more than tripled, to $11 billion. Earnings per share more than tripled too, to over $13. It passed all five of the tool's growth tests. Every single one.

My robot looked at that gorgeous track record and said: bargain. Which is a bit like judging a boxer by the title he won in 2019, while he is, right now, face-down on the canvas.

Here's the part I actually built it for.

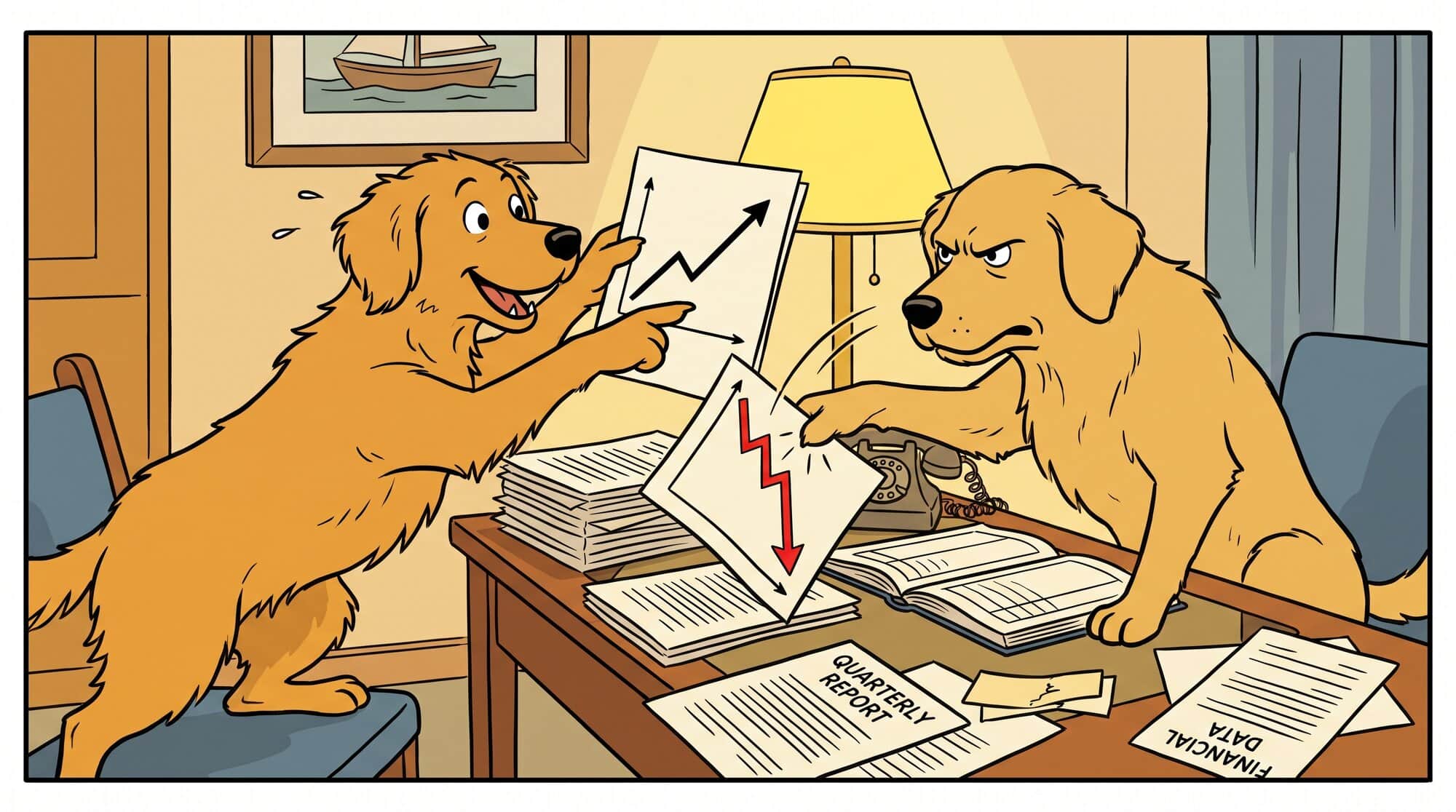

My tool doesn't just hand you a number and a thumbs-up. That's a calculator, and the world has enough of those. This one asks itself about seventy questions, and then argues with itself over every answer — up to four rounds — before it writes a word.

One side is the optimist. It builds the best honest case it can. The other side is a bouncer. Its only job is to be unconvinced. Every time the optimist says something flattering, the bouncer checks it against the real numbers and asks: says who?

On Lululemon, the bouncer would not sit down.

The optimist had honest points. Sales in China had jumped 29% in a year. The brand still prints money.

But the bouncer kept holding up the last three months at home, one page at a time. Profit on each dollar of sales had fallen by more than a third — to 11 cents, from about 18 the year before. Earnings were down 35% in a single quarter. The company had even cut its own forecast for this year — to about $11 a share, down from the $13 it earned last year. Tariffs had taken $275 million last year, with closer to $380 million lined up for this one. And then, almost as an afterthought, the last page: the boss had quit on January 31.

So the report did something I have never seen a spreadsheet do. It talked itself down. The green BUY faded to a yellow wait — not because I told it to, but because its own bouncer wouldn't wave the happy story through.

(It is also slow, and it is not finished. Some days it argues with itself for two and a half hours and then runs out of time mid-sentence. It's a work in progress.)

So: a famous short-seller likes it. A Buffett teacher likes it. My own robot, after a brawl with itself, lands on maybe. That's three votes for paying attention.

I'm going to pass.

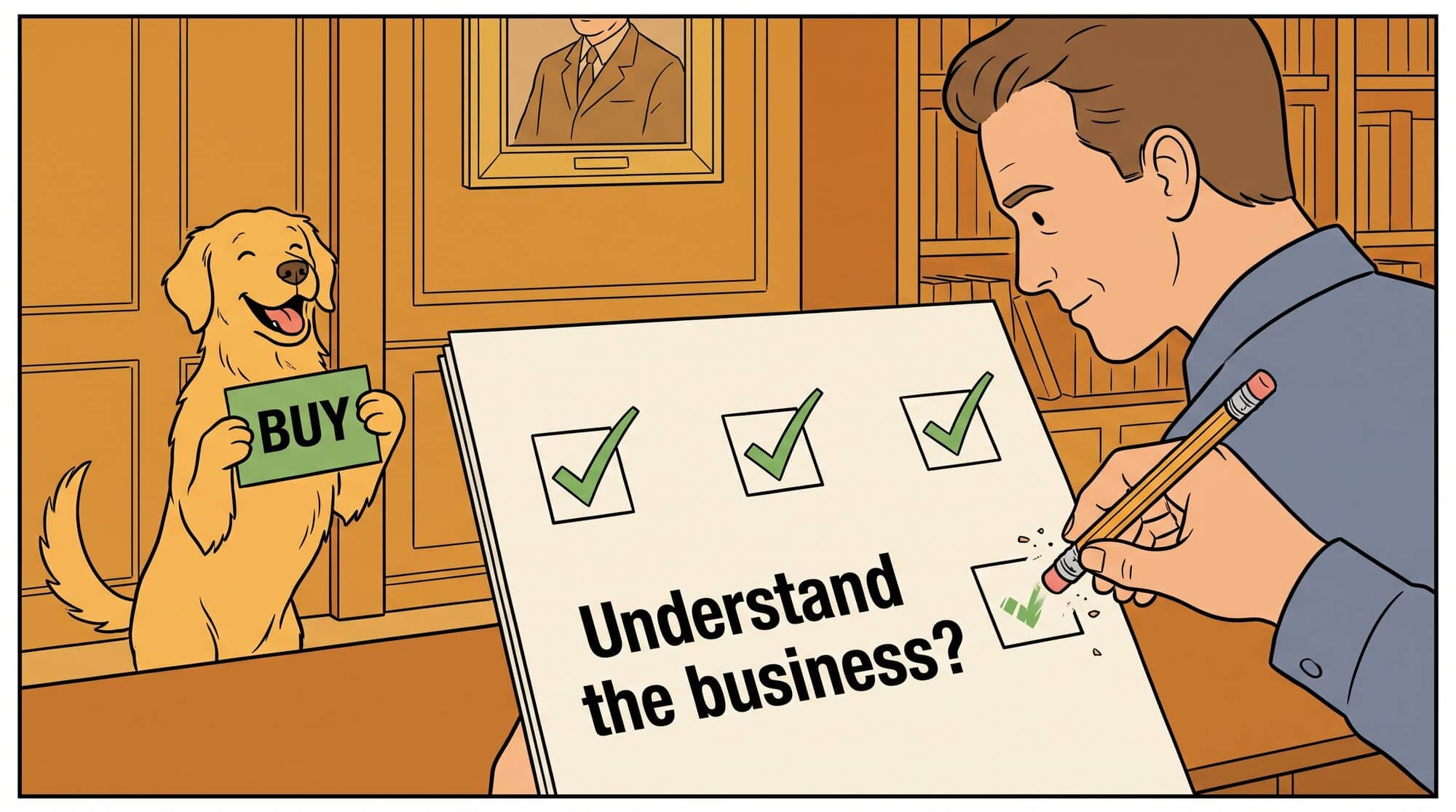

Not because I'm smarter than any of them. I'm plainly not. I pass because of one box on the screen — the box the machine ticked and I unticked.

The box asks, more or less: is this the kind of business you actually understand? The robot ticked yes. It's clothes — how hard can clothes be. And it has a point. But I don't know this world. I don't know whether a $98 legging survives when Costco sells a near-identical one for $7. I don't know if the brand is still cool or quietly turned into your aunt's brand — and the numbers are nervous about it too: among teenage girls, Lululemon slid from the #1 favorite to #3 in a single year, while two rivals you've maybe never heard of came screaming up the list. I don't know if the new boss ends the circus or just joins it. I just don't know.

Warren Buffett has a name for this. He calls it your circle of competence — the short list of things you genuinely understand. The trick isn't having a big circle. The trick is knowing where the edge is, and not lying to yourself about it.

I know software. I've spent years inside it. I do not know leggings. I could learn this business — really learn it, enough to say whether it's worth buying — but I'm not a clothes guy, and never wanted to be. And my machine, for all its reading, can't know that about me. It can tell me what the company is worth on paper. It can't tell me whether I have any business having an opinion.

That turned out to be the most useful thing it gave me all day. Not the price. The nerve to look at a stock down 77%, with three smart parties all saying look closer, and still say the three words you are never supposed to say out loud in finance:

I don't know.

And then close the tab.

Sources

- lululemon athletica inc. — Form 10-K, fiscal 2025 — U.S. Securities and Exchange Commission (EDGAR), filed March 17, 2026. (The annual filing behind the numbers: revenue past $11 billion, diluted earnings of $13.26 a share, China Mainland up 29%, the roughly $275 million gross tariff hit, and CEO Calvin McDonald's departure effective January 31, 2026.)

- lululemon athletica inc. — Q1 fiscal 2026 results (Form 8-K, Exhibit 99.1) — U.S. Securities and Exchange Commission (EDGAR), June 4, 2026. (The quarter that cracked the BUY: earnings per share down about 35%, full-year guidance cut to roughly $11 a share, operating margin down to about 11%.)

- Lululemon (LULU) Q1 2026 Earnings Call Transcript — The Motley Fool, June 4, 2026. (Management's own tariff math — the gross cost rising from about $275 million last year toward roughly $380 million this year, most of it expected to be offset.)

- lululemon athletica inc. (LULU) — stock price history — StockAnalysis.com. (The fall: from the late-December 2023 high near $511 to roughly $117 — down about 77%.)

- Lululemon beats on Q1 2025 earnings, cuts outlook — CNBC, June 5, 2025. (The guidance cut that knocked the stock down about 20% in a single day last June.)

- lululemon athletica (LULU): An Ode to Bad Management & The Politics of Skin-Tight Leggings — Michael Burry, Cassandra Unchained (Substack), June 2026. (The bull case: the one U.S. clothing company of any market capitalization trading at under ten times earnings, and the line "bad management is a value investor's best friend.")

- About Phil Town — Rule #1 Investing — Rule One Investing. (The "fellow who teaches regular people to invest like Warren Buffett," and the sticker-price / margin-of-safety method the tool's math mirrors.)

- The Lululemon Chip Wilson Comments Controversy, Explained — TODAY, January 8, 2024. (The founder circus: the 2013 see-through-pants recall, the "some women's bodies just don't actually work" interview, and the apology he gave to employees rather than to the women.)

- Lululemon accuses Costco of selling 'unauthorized' versions of its $128 pants — CNN Business, June 30, 2025. (The dupe problem in one lawsuit: near-identical store-brand leggings sold for a small fraction of Lululemon's price.)

- Piper Sandler Survey Reveals Nike, Lululemon and Stanley Losing Teen Mindshare — SGB Media. (The "Taking Stock With Teens" finding behind the rank slip from #1 to #3 in a year, with Alo and Vuori climbing.)

- Berkshire Hathaway — Chairman's Letter, 1996 — Warren Buffett, 1996. (The source of "circle of competence": the size of the circle isn't what matters — knowing its boundary is.)

- The Machine Is Not Allowed to Sign the Checks — Conny Lazo, June 12, 2026. (The companion argument: the tool can price and recommend; the human keeps the decision.)

- I Wrote Intel's Comeback Story. Then I Asked My Tool What It Was Worth. — Conny Lazo, June 17, 2026. (The same tool reaching a "too hard" verdict — value investing as a reason to walk away.)